Opening an Indexed Universal Life (IUL) insurance policy often involves costs, but you might be wondering How To Open A Iul Account For Free. Let’s delve into the realities of IUL costs and explore strategies to minimize expenses.

Understanding IUL Costs: Is “Free” Realistic?

While the idea of a completely “free” IUL account is generally unrealistic, understanding the various costs associated with IUL policies can empower you to make informed decisions and potentially minimize your out-of-pocket expenses. IUL policies aren’t free because they combine life insurance coverage with a cash value component that grows based on market index performance.

Key IUL Expenses

Several factors contribute to the overall cost of an IUL policy. These include:

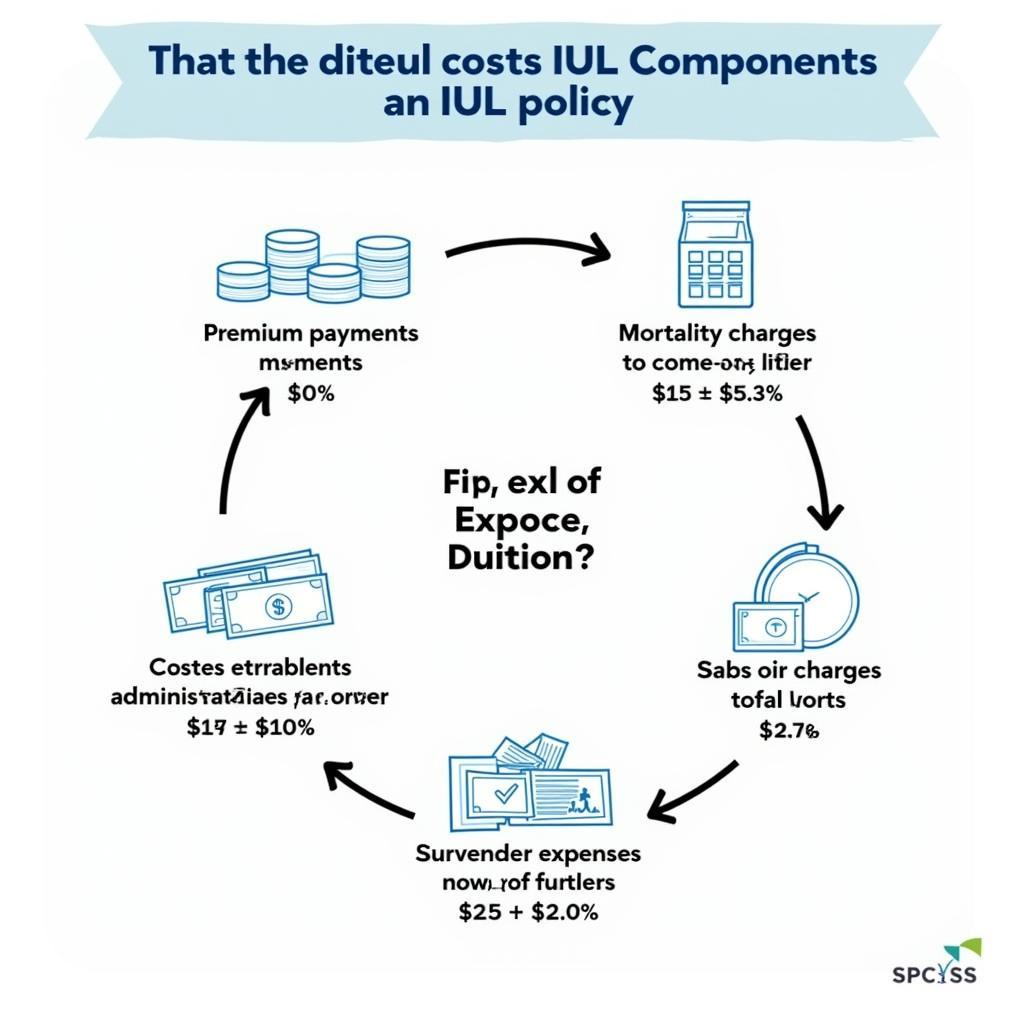

- Premium Payments: The most significant cost is the regular premium you pay to keep the policy active. This premium covers both the cost of insurance and contributes to the cash value accumulation.

- Mortality Charges: These charges cover the cost of the life insurance benefit and are deducted from the cash value. They vary based on factors like age, health, and coverage amount.

- Administrative Expenses: These cover the insurer’s operational costs and are typically deducted from the cash value.

- Cost of Riders: Optional riders, such as long-term care coverage, add to the overall policy cost.

- Surrender Charges: If you surrender the policy early, you might incur surrender charges, which can significantly impact the cash value you receive.

IUL Costs Breakdown

IUL Costs Breakdown

Strategies to Minimize IUL Costs

While a truly “free” IUL account is unlikely, you can employ strategies to optimize your policy and reduce costs.

Shop Around and Compare Quotes

Different insurance companies offer varying premium rates, fees, and policy features. Comparing quotes from multiple insurers allows you to identify the most competitive and cost-effective options.

Negotiate with Insurers

Don’t be afraid to negotiate with insurers. Sometimes, they are willing to adjust premium rates or fees to secure your business.

Optimize Premium Payments

Carefully consider your premium payment amount. A higher premium may lead to faster cash value growth, but it also means higher upfront costs. Find a balance that aligns with your financial goals and budget.

Review Policy Regularly

Regularly review your IUL policy to ensure it still aligns with your needs and financial objectives. As your circumstances change, you might be able to adjust your policy to optimize its cost-effectiveness.

Is a “No-Load” IUL a Free Option?

Some companies offer “no-load” IUL policies, which eliminate or reduce upfront sales commissions. While this can lower initial costs, it’s crucial to examine the policy’s overall fees and expenses, as they might be higher in other areas. “No-load” doesn’t mean “free,” so carefully compare all costs.

Expert Insight: John Smith, Certified Financial Planner

“While ‘no-load’ IULs might sound appealing due to lower upfront commissions, it’s essential to look beyond the initial cost and evaluate the long-term expenses associated with the policy. A thorough comparison with traditional IUL policies is crucial.”

Conclusion

While a completely free IUL account is generally unattainable, understanding the costs associated with IUL policies and implementing cost-minimization strategies can help you make informed decisions and optimize your investment. Remember, comparing quotes, negotiating with insurers, and regularly reviewing your policy are crucial steps in maximizing the value of your IUL. How to open a IUL account for free, in the truest sense, may be impossible, but smart planning can make it more affordable.

FAQ

- What is an IUL?

- How does the cash value component of an IUL work?

- What are the main costs associated with an IUL policy?

- Can I withdraw money from my IUL’s cash value?

- What are the tax implications of an IUL?

- What are the benefits of an IUL compared to other life insurance policies?

- How can I find a reputable IUL provider?

Need Help?

Contact us: Phone Number: 0972669017, Email: [email protected] or visit us at 142 Trần Nhân Tông, Yên Thanh, Uông Bí, Quảng Ninh, Vietnam. We have a 24/7 customer support team.